Keltner channel LE not working correctly?

I am trying to run the Keltner channel strategy that goes long when price closes above the upper band and sells when price closes below lower band. Basically the default Keltner LE and SE. However, when looking at the order on the exchange, I see that the buy stop has been set to a price a lot higher than the Keltner channel lines on the chart. I have put a screenshot to show you what I mean. What am I doing wrong?

- Attachments

-

- keltner_screenshot.png

- (24.56 KiB) Not downloaded yet

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

First, a few questions to understand:

Are you using the original Multicharts signal?

Or have you modified them?

Do you have a problem setting the stop buy order or executing it?

From your picture I would assume that the stop buy has only been placed but not yet executed.

and why is the stop order named stop loss? Do you want to make a new long entry or close your short entry?

When exactly was the stop placed? Add the attached line of code: directly above your buy order code line, then you should be able to see in the chart when the order was generated, perhaps this will increase your/my understanding of the problem.

In the original code, an offset of 1pip is used for the stop order. The execution itself can also take place later after the stop has been triggered. And as far as I know, the stop order then becomes a market order that is executed at the next available price. This can also be significantly higher.

Are you using the original Multicharts signal?

Or have you modified them?

Do you have a problem setting the stop buy order or executing it?

From your picture I would assume that the stop buy has only been placed but not yet executed.

and why is the stop order named stop loss? Do you want to make a new long entry or close your short entry?

When exactly was the stop placed? Add the attached line of code: directly above your buy order code line, then you should be able to see in the chart when the order was generated, perhaps this will increase your/my understanding of the problem.

Code: Select all

DrwArrow.Create(new ChartPoint(Bars.CurrentBar, Bars.High.Value), true);In the original code, an offset of 1pip is used for the stop order. The execution itself can also take place later after the stop has been triggered. And as far as I know, the stop order then becomes a market order that is executed at the next available price. This can also be significantly higher.

Thank you for the quick reply.First, a few questions to understand:

Are you using the original Multicharts signal?

Or have you modified them?

Do you have a problem setting the stop buy order or executing it?

From your picture I would assume that the stop buy has only been placed but not yet executed.

and why is the stop order named stop loss? Do you want to make a new long entry or close your short entry?

When exactly was the stop placed? Add the attached line of code: directly above your buy order code line, then you should be able to see in the chart when the order was generated, perhaps this will increase your/my understanding of the problem.

Code: Select all

DrwArrow.Create(new ChartPoint(Bars.CurrentBar, Bars.High.Value), true);

In the original code, an offset of 1pip is used for the stop order. The execution itself can also take place later after the stop has been triggered. And as far as I know, the stop order then becomes a market order that is executed at the next available price. This can also be significantly higher.

1. I am using the original signal provided by Multicharts.

2.The problem is not the placing or execution but the location/price of the stop buy.

3. It would be the new long entry

4. Stop is placed as soon as I turn on automated trading

Does the 1pip offset work for crypto?

I dont think I understand how the signal is supposed to work. My understanding was that it goes long when the price closes above the upper band and sells when price closes below lower band. I don't understand why its placing a stop buy in the first place, and if it is, why that stop buy is so far from the upper keltner band.

Last edited by Kghiasv on Aug 09 2024, edited 1 time in total.

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

ah, ok, so the stop is only misplaced once when you switch to automatic trading? and then no more?

I'll take another look, I'm currently updating Multicharts.

i think your right: https://www.multicharts.com/trading-sof ... Channel_LE

I'll take another look, I'm currently updating Multicharts.

i think your right: https://www.multicharts.com/trading-sof ... Channel_LE

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

I think it may be due to the transition from backtesting to automatic trading. Someone here recently had a problem like this, so can you answer my question, does this also occur with subsequent orders?

Is the problem with the 1 point above the high then? As in, is the problem because the 1 point system doesn't work with crypto?ah, ok, so the stop is only misplaced once when you switch to automatic trading? and then no more?

I'll take another look, I'm currently updating Multicharts.

i think your right: https://www.multicharts.com/trading-sof ... Channel_LE

What do you mean by subsequent orders? Are you asking if it happens with every order?I think it may be due to the transition from backtesting to automatic trading. Someone here recently had a problem like this, so can you answer my question, does this also occur with subsequent orders?

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

I mean: when you turn on automated trading, the stop order is generated immediately?

I'm wondering about the name of the stop. Do you have any other signals or indicators active?

For me it is called “KltChLE”, at least in the back test.

Therefore my question was whether if the stop order was reached once and then a new stop order was generated, whether it would also be placed incorrectly.

I suspect that the stop order does not come from the Keltner channel, but either from the backtest or from another strategy

If you insert the line of code I mentioned, you should be able to see whether the stop order comes from the keltnerchanel LE.

I'm wondering about the name of the stop. Do you have any other signals or indicators active?

For me it is called “KltChLE”, at least in the back test.

Therefore my question was whether if the stop order was reached once and then a new stop order was generated, whether it would also be placed incorrectly.

I suspect that the stop order does not come from the Keltner channel, but either from the backtest or from another strategy

If you insert the line of code I mentioned, you should be able to see whether the stop order comes from the keltnerchanel LE.

- Attachments

-

- 4.png

- (514.2 KiB) Not downloaded yet

I only have the keltner channel signals applied.I mean: when you turn on automated trading, the stop order is generated immediately?

I'm wondering about the name of the stop. Do you have any other signals or indicators active?

For me it is called “KltChLE”, at least in the back test.

Therefore my question was whether if the stop order was reached once and then a new stop order was generated, whether it would also be placed incorrectly.

I suspect that the stop order does not come from the Keltner channel, but either from the backtest or from another strategy

When I turn on automated trading in portfolio manager, I see that the stop order is placed on the exchange immediately. Also, the screen shot I sent was non executed stop buy order on the exchange and not Multicharts so that is probably why it has a different name.

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

viewtopic.php?t=54379

I wonder if you have the same problem as described in the following forum post. If so, you should actually contact the live chat, as this seems to be a common problem. Perhaps Multicharts can then integrate automatic deletion of old "backtest orders" as a function into Multicharts.

I wonder if you have the same problem as described in the following forum post. If so, you should actually contact the live chat, as this seems to be a common problem. Perhaps Multicharts can then integrate automatic deletion of old "backtest orders" as a function into Multicharts.

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

Based on your new description, I can't yet rule out whether it's a multicharts/indicator or a broker problem. Of course I can only help with programming problems in Multicharts. Otherwise someone from multicharts has to answer here or you go to the live chat.I only have the keltner channel signals applied.I mean: when you turn on automated trading, the stop order is generated immediately?

I'm wondering about the name of the stop. Do you have any other signals or indicators active?

For me it is called “KltChLE”, at least in the back test.

Therefore my question was whether if the stop order was reached once and then a new stop order was generated, whether it would also be placed incorrectly.

I suspect that the stop order does not come from the Keltner channel, but either from the backtest or from another strategy

When I turn on automated trading in portfolio manager, I see that the stop order is placed on the exchange immediately. Also, the screen shot I sent was non executed stop buy order on the exchange and not Multicharts so that is probably why it has a different name.

In the back test it shows up as KltChLE. I added the arrow script and the arrow says it was supposed to be long at the upper band as I thought. The issue seems to be the offset of the order. I have contacted support and sent them the information they needed.Based on your new description, I can't yet rule out whether it's a multicharts/indicator or a broker problem. Of course I can only help with programming problems in Multicharts. Otherwise someone from multicharts has to answer here or you go to the live chat.I only have the keltner channel signals applied.I mean: when you turn on automated trading, the stop order is generated immediately?

I'm wondering about the name of the stop. Do you have any other signals or indicators active?

For me it is called “KltChLE”, at least in the back test.

Therefore my question was whether if the stop order was reached once and then a new stop order was generated, whether it would also be placed incorrectly.

I suspect that the stop order does not come from the Keltner channel, but either from the backtest or from another strategy

When I turn on automated trading in portfolio manager, I see that the stop order is placed on the exchange immediately. Also, the screen shot I sent was non executed stop buy order on the exchange and not Multicharts so that is probably why it has a different name.

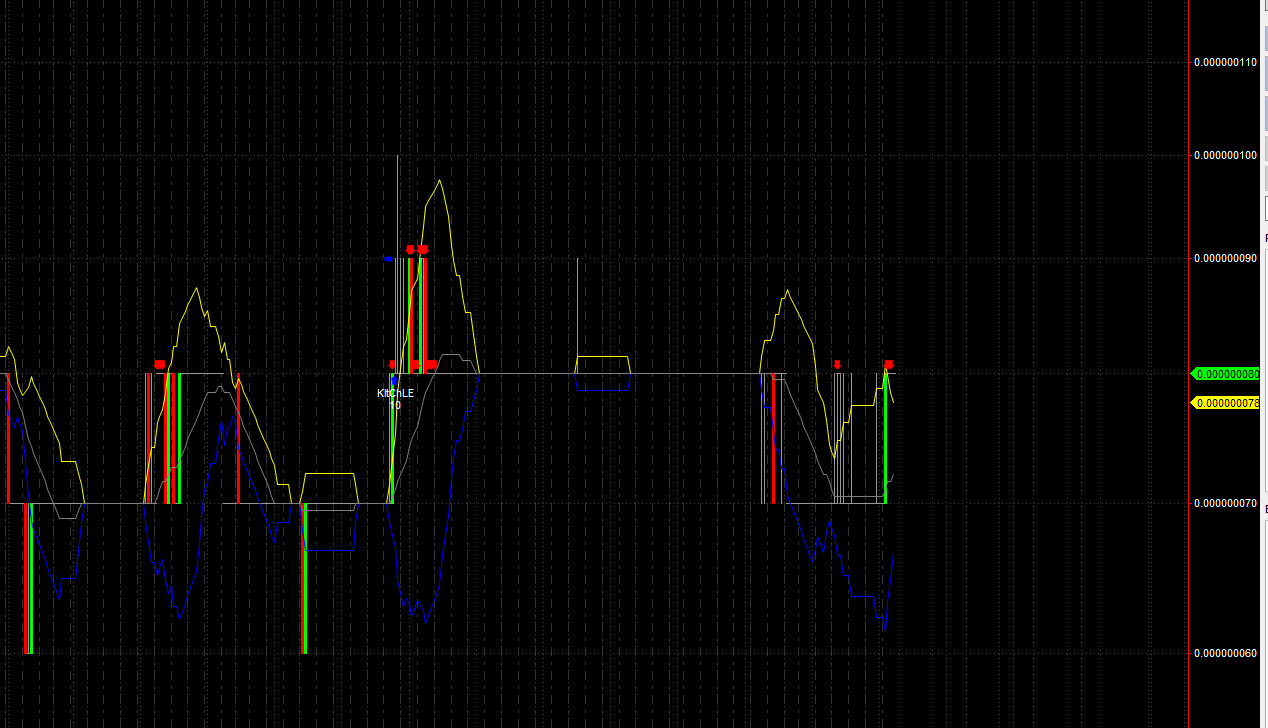

The arrows indicate that the stop should be executed around the yellow upper band

https://i.gyazo.com/7d5833c1daf91f16ac8 ... a1432e.png

What happens though is that the order gets submitted significantly higher than the upper band. See attached image.

https://i.gyazo.com/7d5833c1daf91f16ac8 ... a1432e.png

{kind=link}

What happens though is that the order gets submitted significantly higher than the upper band. See attached image.

- Attachments

-

- keltner_screenshot.png

- (24.59 KiB) Not downloaded yet

It might be what you're saying as the location of the buy stop is the location of the last back tested trade.viewtopic.php?t=54379

I wonder if you have the same problem as described in the following forum post. If so, you should actually contact the live chat, as this seems to be a common problem. Perhaps Multicharts can then integrate automatic deletion of old "backtest orders" as a function into Multicharts.

Prior to finding the reference to my own thread (Rogue trades) I already thought to respond. So regarding the subject in this thread here (Keltner channel etc.) I hope to contribute with this :

The activation of Autotrading goes in a way which is (for me) weird, to say the least. First thing what happens (or seem to happen) is that from the moment you activate Autotrading, all the bars in the cache will be traversed for a reason unknown. My idea about it is that first the "backtesting" part is executed, and when finally the current bars are reached, Autotrading may commence for real. If you'd observe the CPU usage, you will know when this "preprocess" is finished (it consumes a lot more CPU than when all is ready to go).

Let me add that my Autotrading does not wait even one second before a position is opened - it does that right away. This allows to judge "anomaly" quite well.

Now here is where this "knowledge" meets the issue described in this thread :

At some stage the broker opens the position. This is always the first trade visible, and this is not the Strategy's trade. This is always later and when exactly is not clear to me, but later. This could be "minutes". Now, because I work in AA (Asynchronous) mode, this allows for this situation in the first place (with AS mode Broker and Strategy entries would occur at the same moment). But now the thing :

When the Strategy finally enters its own trade (with the notice that all the time Broker matches Strategy already (in the Order and Position Tracker)), this occurs at the price of the moment; would this price be higher (for a Long) then the Strategy only then starts to update its Currentosition.OpenProfit and thus the trade remains open longer than the Broker position would account for. This is how a first trade always is "off" with usually a much higher profit (this would be inherent for the Long position which starts like that for a reason (trend). Fact is :

This is incorrect.

What I now envision is that a SL etc. (formal TP too) would be submitted immediately while in your case (AS mode assumed) the real Entry is similar to what I encounter : thus later, when in my case the Strategy would enter.

The whole thing seems too complicated to even begin announcing it as bug (because how to mimic it, unless with real trading), but someone over at MC should be able to reason it out.

In addition, I feel that this is related to how the EnvironmentIsRealTimeCalc does its thing, which you don't need to be using in the first place. After days and days of observing this all, I now think that this property (or function) switches to True once the real Autotrading commenced (which is in my case when the Broker trade enters). This property / function lags because of the ticks (could be 10K ticks per second) *AND* the system is again disturbed by high CPU usage when the Autotrading commences (this higher CPU usage will settle down).

I did not work on the solution of this issue, because it is all with very indirect effects. But I already do know about some other way around : if I replace in my very case the EnvironmentIsRealTimeCalc with my self-made IsProd (read as IsLive) then no trade ever occurs. Also, referring to that other (Rogue) thread I am by now pretty much 100% sure that over there the same thing is happening, which is why I simply miss the start of it all and which is why I can't interfere with it. This is hard to explain, but the proper Output.Write tells it all easily. Thus, things occur during live trading, while the MC engine does not call the CalcBar() yet. The Rogue thing I solved, and for this SL etc. I would try to approach it the same.

My guts tell me that if you put the SL etc. under the condition of EnvironmentIsRealTimeCalc (True) that you will get there.

Ah, what helped me too is building in a System.Threading.Thread.Sleep(2000) before I start to do real things. This is to be build in CalcBar() (not in StartCalc) and of course only to be executed once (If "Initializing" and such). That at least allows me to show a "Start" entry in the Editor output and see things from the real beginning of the CalcBar calls.

Summarized (sort of)

Try to envision that you have conditions under If EnvironmentIsRealTimeCalc and that when you start Autotrading, all the bars in there are being processed with this property being false, until the current bar is reached. Then still all kind of arrangements have to be made, until finally this property gets true and you can formally do your thing (like putting SL/TP pending orders). In AA mode all is still vague, but I think in SA mode this should to the job decently. Do please notice that when all the bars have been processed (I deem this a necessity - so I accept that), it still will take many minutes before the first real trade occurs. You might think your conditions are not met for several minutes, but I jump in right away and thus can see it is not right (or at least it requires understanding which I can't yet).

Please respond with your own judgment and further findings, so we can hopefully all learn from it. Your issue and me writing about it helps myself as well.

The activation of Autotrading goes in a way which is (for me) weird, to say the least. First thing what happens (or seem to happen) is that from the moment you activate Autotrading, all the bars in the cache will be traversed for a reason unknown. My idea about it is that first the "backtesting" part is executed, and when finally the current bars are reached, Autotrading may commence for real. If you'd observe the CPU usage, you will know when this "preprocess" is finished (it consumes a lot more CPU than when all is ready to go).

Let me add that my Autotrading does not wait even one second before a position is opened - it does that right away. This allows to judge "anomaly" quite well.

Now here is where this "knowledge" meets the issue described in this thread :

At some stage the broker opens the position. This is always the first trade visible, and this is not the Strategy's trade. This is always later and when exactly is not clear to me, but later. This could be "minutes". Now, because I work in AA (Asynchronous) mode, this allows for this situation in the first place (with AS mode Broker and Strategy entries would occur at the same moment). But now the thing :

When the Strategy finally enters its own trade (with the notice that all the time Broker matches Strategy already (in the Order and Position Tracker)), this occurs at the price of the moment; would this price be higher (for a Long) then the Strategy only then starts to update its Currentosition.OpenProfit and thus the trade remains open longer than the Broker position would account for. This is how a first trade always is "off" with usually a much higher profit (this would be inherent for the Long position which starts like that for a reason (trend). Fact is :

This is incorrect.

What I now envision is that a SL etc. (formal TP too) would be submitted immediately while in your case (AS mode assumed) the real Entry is similar to what I encounter : thus later, when in my case the Strategy would enter.

The whole thing seems too complicated to even begin announcing it as bug (because how to mimic it, unless with real trading), but someone over at MC should be able to reason it out.

In addition, I feel that this is related to how the EnvironmentIsRealTimeCalc does its thing, which you don't need to be using in the first place. After days and days of observing this all, I now think that this property (or function) switches to True once the real Autotrading commenced (which is in my case when the Broker trade enters). This property / function lags because of the ticks (could be 10K ticks per second) *AND* the system is again disturbed by high CPU usage when the Autotrading commences (this higher CPU usage will settle down).

I did not work on the solution of this issue, because it is all with very indirect effects. But I already do know about some other way around : if I replace in my very case the EnvironmentIsRealTimeCalc with my self-made IsProd (read as IsLive) then no trade ever occurs. Also, referring to that other (Rogue) thread I am by now pretty much 100% sure that over there the same thing is happening, which is why I simply miss the start of it all and which is why I can't interfere with it. This is hard to explain, but the proper Output.Write tells it all easily. Thus, things occur during live trading, while the MC engine does not call the CalcBar() yet. The Rogue thing I solved, and for this SL etc. I would try to approach it the same.

My guts tell me that if you put the SL etc. under the condition of EnvironmentIsRealTimeCalc (True) that you will get there.

Ah, what helped me too is building in a System.Threading.Thread.Sleep(2000) before I start to do real things. This is to be build in CalcBar() (not in StartCalc) and of course only to be executed once (If "Initializing" and such). That at least allows me to show a "Start" entry in the Editor output and see things from the real beginning of the CalcBar calls.

Summarized (sort of)

Try to envision that you have conditions under If EnvironmentIsRealTimeCalc and that when you start Autotrading, all the bars in there are being processed with this property being false, until the current bar is reached. Then still all kind of arrangements have to be made, until finally this property gets true and you can formally do your thing (like putting SL/TP pending orders). In AA mode all is still vague, but I think in SA mode this should to the job decently. Do please notice that when all the bars have been processed (I deem this a necessity - so I accept that), it still will take many minutes before the first real trade occurs. You might think your conditions are not met for several minutes, but I jump in right away and thus can see it is not right (or at least it requires understanding which I can't yet).

Please respond with your own judgment and further findings, so we can hopefully all learn from it. Your issue and me writing about it helps myself as well.

Thank you for the response. I have emailed support and am in the stage of trying to replicate the issue for the logs.Prior to finding the reference to my own thread (Rogue trades) I already thought to respond. So regarding the subject in this thread here (Keltner channel etc.) I hope to contribute with this :

The activation of Autotrading goes in a way which is (for me) weird, to say the least. First thing what happens (or seem to happen) is that from the moment you activate Autotrading, all the bars in the cache will be traversed for a reason unknown. My idea about it is that first the "backtesting" part is executed, and when finally the current bars are reached, Autotrading may commence for real. If you'd observe the CPU usage, you will know when this "preprocess" is finished (it consumes a lot more CPU than when all is ready to go).

Let me add that my Autotrading does not wait even one second before a position is opened - it does that right away. This allows to judge "anomaly" quite well.

Now here is where this "knowledge" meets the issue described in this thread :

At some stage the broker opens the position. This is always the first trade visible, and this is not the Strategy's trade. This is always later and when exactly is not clear to me, but later. This could be "minutes". Now, because I work in AA (Asynchronous) mode, this allows for this situation in the first place (with AS mode Broker and Strategy entries would occur at the same moment). But now the thing :

When the Strategy finally enters its own trade (with the notice that all the time Broker matches Strategy already (in the Order and Position Tracker)), this occurs at the price of the moment; would this price be higher (for a Long) then the Strategy only then starts to update its Currentosition.OpenProfit and thus the trade remains open longer than the Broker position would account for. This is how a first trade always is "off" with usually a much higher profit (this would be inherent for the Long position which starts like that for a reason (trend). Fact is :

This is incorrect.

What I now envision is that a SL etc. (formal TP too) would be submitted immediately while in your case (AS mode assumed) the real Entry is similar to what I encounter : thus later, when in my case the Strategy would enter.

The whole thing seems too complicated to even begin announcing it as bug (because how to mimic it, unless with real trading), but someone over at MC should be able to reason it out.

In addition, I feel that this is related to how the EnvironmentIsRealTimeCalc does its thing, which you don't need to be using in the first place. After days and days of observing this all, I now think that this property (or function) switches to True once the real Autotrading commenced (which is in my case when the Broker trade enters). This property / function lags because of the ticks (could be 10K ticks per second) *AND* the system is again disturbed by high CPU usage when the Autotrading commences (this higher CPU usage will settle down).

I did not work on the solution of this issue, because it is all with very indirect effects. But I already do know about some other way around : if I replace in my very case the EnvironmentIsRealTimeCalc with my self-made IsProd (read as IsLive) then no trade ever occurs. Also, referring to that other (Rogue) thread I am by now pretty much 100% sure that over there the same thing is happening, which is why I simply miss the start of it all and which is why I can't interfere with it. This is hard to explain, but the proper Output.Write tells it all easily. Thus, things occur during live trading, while the MC engine does not call the CalcBar() yet. The Rogue thing I solved, and for this SL etc. I would try to approach it the same.

My guts tell me that if you put the SL etc. under the condition of EnvironmentIsRealTimeCalc (True) that you will get there.

Ah, what helped me too is building in a System.Threading.Thread.Sleep(2000) before I start to do real things. This is to be build in CalcBar() (not in StartCalc) and of course only to be executed once (If "Initializing" and such). That at least allows me to show a "Start" entry in the Editor output and see things from the real beginning of the CalcBar calls.

Summarized (sort of)

Try to envision that you have conditions under If EnvironmentIsRealTimeCalc and that when you start Autotrading, all the bars in there are being processed with this property being false, until the current bar is reached. Then still all kind of arrangements have to be made, until finally this property gets true and you can formally do your thing (like putting SL/TP pending orders). In AA mode all is still vague, but I think in SA mode this should to the job decently. Do please notice that when all the bars have been processed (I deem this a necessity - so I accept that), it still will take many minutes before the first real trade occurs. You might think your conditions are not met for several minutes, but I jump in right away and thus can see it is not right (or at least it requires understanding which I can't yet).

Please respond with your own judgment and further findings, so we can hopefully all learn from it. Your issue and me writing about it helps myself as well.

Regarding the code, so just add Environment.IsRealTimeCalc like this?

Code: Select all

if (m_bSetupLE.Value && Environment.IsRealTimeCalc)

m_KltChLE.Send(m_CrossingHigh.Value + Bars.Point);(very) Generally I would put all the code under the IsRealTimeCalc condition. So all would be done in Backtesting mode, or all would be in Live Trading mode. In other words, be careful that you are not assigning value to variables throughout the processing of the backtesting part, which may have an inconsistent influence on the Live part of the process.

Btw, the "preprocess" of Backtesting when activating the Strategy is formal and written in the Programming Manual on paragraph 4.6.5 (found that myself yesterday). Why this is per se done like that, I don't know.

Edit :

Above is too simple, because it would not allow backtesting any more;

You can create an Input Variable e.g. Prod, and set that to true when you want to go Live. The code would then be subject to

Btw, the "preprocess" of Backtesting when activating the Strategy is formal and written in the Programming Manual on paragraph 4.6.5 (found that myself yesterday). Why this is per se done like that, I don't know.

Edit :

Above is too simple, because it would not allow backtesting any more;

You can create an Input Variable e.g. Prod, and set that to true when you want to go Live. The code would then be subject to

Code: Select all

if (!Prod || (Prod && Environment.IsRealTimeCalc))I added an input for prod but can't figure out where to put the line of code at the top without it giving errors. Do I put it before using System?(very) Generally I would put all the code under the IsRealTimeCalc condition. So all would be done in Backtesting mode, or all would be in Live Trading mode. In other words, be careful that you are not assigning value to variables throughout the processing of the backtesting part, which may have an inconsistent influence on the Live part of the process.

Btw, the "preprocess" of Backtesting when activating the Strategy is formal and written in the Programming Manual on paragraph 4.6.5 (found that myself yesterday). Why this is per se done like that, I don't know.

Edit :

Above is too simple, because it would not allow backtesting any more;

You can create an Input Variable e.g. Prod, and set that to true when you want to go Live. The code would then be subject toCode: Select all

if (!Prod || (Prod && Environment.IsRealTimeCalc))

Code: Select all

using System;

using PowerLanguage.Function;

namespace PowerLanguage.Strategy

{

[IOGMode(IOGMode.Disabled)]

public class Keltner_Channel_LE : SignalObject

{

private AverageFC m_AverageFC;

private VariableSeries<Double> m_UpperBand;

private VariableObject<Boolean> m_bSetupLE;

private VariableObject<Double> m_CrossingHigh;

private IOrderPriced m_KltChLE;

public Keltner_Channel_LE(object ctx) :

base(ctx){

NumAtrs = 1.5;

Length = 20;

}

private ISeries<double> Price { get; set; }

[Input]

public int Length { get; set; }

[Input]

public double NumAtrs { get; set; }

[Input]

public bool Prod{ get; set; }

protected override void Create(){

m_AverageFC = new AverageFC(this);

m_UpperBand = new VariableSeries<Double>(this);

m_bSetupLE = new VariableObject<bool>(this);

m_CrossingHigh = new VariableObject<double>(this);

m_KltChLE = OrderCreator.Stop(new SOrderParameters(Contracts.Default, "KltChLE", EOrderAction.Buy));

}

protected override void StartCalc(){

Price = Bars.Close;

m_AverageFC.price = Price;

m_AverageFC.length = Length;

}

protected override void CalcBar(){

double m_avg = m_AverageFC[0];

double m_shift = NumAtrs*this.AverageTrueRange(Length);

m_UpperBand.Value = m_avg + m_shift;

if (Bars.CurrentBar > 1 && Price.CrossesOver(m_UpperBand, ExecInfo.MaxBarsBack))

{

m_bSetupLE.Value = true;

m_CrossingHigh.Value = Bars.High[0];

}

else{

if (m_bSetupLE.Value

&& (PublicFunctions.DoubleLess(Price[0], m_avg)

|| PublicFunctions.DoubleGreaterEquals(Bars.High[0], m_CrossingHigh.Value + Bars.Point)))

m_bSetupLE.Value = false;

}

if (m_bSetupLE.Value)

m_KltChLE.Send(m_CrossingHigh.Value + Bars.Point);

}

}

}

Code: Select all

protected override void CalcBar()

{

// N.b.: The If below is slightly different than

// in my previous post but will do too.

// But now all the "preprocessing" backtest stuff

// will not occur in Live.

if (!Prod || Environment.IsRealTimeCalc) // !Prod = Backtesting.

{

// All of your code to be executed per Bar goes here.

}

}

Of course don't forget to set Prod to True when you apply the Strategy to Live.

Yes thank you. I think the issue has been fixed now but will have to see it take a signal to be sure. Will let you know when I find out.Clear a little now ?Code: Select all

protected override void CalcBar() { // N.b.: The If below is slightly different than // in my previous post but will do too. // But now all the "preprocessing" backtest stuff // will not occur in Live. if (!Prod || Environment.IsRealTimeCalc) // !Prod = Backtesting. { // All of your code to be executed per Bar goes here. } }

Of course don't forget to set Prod to True when you apply the Strategy to Live.

The fact that MC herself does not respond in threads like these, really does not help.

An extension to the anomalies I encounter myself regarding this, is skipping (hence apply a return) all the bars/calls which are beyond the current date and time. Pseudo code :

**): an Input of the time today which is e.g. 3 minutes past when you start the Strategy, allowing for all the bars in the cache to be skipped up to the current point in time.

I can't tell how this cooperates with your situation of necessary preloaded bars for calculating averages etc. which may require x minutes as well, and which must be allowed to calculate.

Again I realize how vague this all is to explain. But it is MC who needs to have their act together in the first place. I can only hope this helps you.

An extension to the anomalies I encounter myself regarding this, is skipping (hence apply a return) all the bars/calls which are beyond the current date and time. Pseudo code :

Code: Select all

if (Bars.DateTime < DateTimeOfInput) // DateTimeOfInput = **

return;I can't tell how this cooperates with your situation of necessary preloaded bars for calculating averages etc. which may require x minutes as well, and which must be allowed to calculate.

Again I realize how vague this all is to explain. But it is MC who needs to have their act together in the first place. I can only hope this helps you.

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

The fact that MC herself does not respond in threads like these, really does not help.

An extension to the anomalies I encounter myself regarding this, is skipping (hence apply a return) all the bars/calls which are beyond the current date and time. Pseudo code :

**): an Input of the time today which is e.g. 3 minutes past when you start the Strategy, allowing for all the bars in the cache to be skipped up to the current point in time.Code: Select all

if (Bars.DateTime < DateTimeOfInput) // DateTimeOfInput = ** return;

I can't tell how this cooperates with your situation of necessary preloaded bars for calculating averages etc. which may require x minutes as well, and which must be allowed to calculate.

Again I realize how vague this all is to explain. But it is MC who needs to have their act together in the first place. I can only hope this helps you.

Code: Select all

//

// Zusammenfassung:

// This method is called every tick from the calculation's beginning bar until the

// last historical bar.

//

// Every real-time tick (or bar close, optionally) after the historical calculation.

protected abstract void CalcBar();

//

// Zusammenfassung:

// Allows control of mouse-click events on the chart.

//

// Parameter:

// arg:

// Specifies the mouse-click parameters. Keyboard button code, mouse button code,

// chart point, bar number and data stream number parameters are passed.

protected virtual void OnMouseEvent(MouseClickArgs arg)

{

CalcBar();

}

//

// Zusammenfassung:

// Event that occurs after strategy Order has been Filled at broker. This method

// can be used only for automated trading, not for manual trading.

protected virtual void OnBrokerStategyOrderFilled([MarshalAs(UnmanagedType.U1)] bool is_buy, int quantity, double avg_fill_price)

{

CalcBar();

}

//

// Zusammenfassung:

// Event that occurs after MarketPosition and/or average Entry Price changed at

// broker.

protected virtual void OnBrokerPositionChange()

{

CalcBar();

}

//

// Zusammenfassung:

// Event that happens after timeout in RecalcLastBarAfter function occurs.

protected virtual void OnRecalcLastBarAfterEvent()

{

CalcBar();

}

//

// Zusammenfassung:

// Event that happens after the Close Position button is pressed in Portfolio Trader

protected virtual void OnUserClickClosePositionButtonEvent()

{

CalcBar();

}This is what support said:

We have analyzed the issue.

I’m afraid, in MultiCharts it is not possible to trade SCXBT since its price scale is smaller than the minimum one supported in MultiCharts (0.000000001).

We are considering implementing smaller price scales in one of the future versions of MultiCharts.

We have analyzed the issue.

I’m afraid, in MultiCharts it is not possible to trade SCXBT since its price scale is smaller than the minimum one supported in MultiCharts (0.000000001).

We are considering implementing smaller price scales in one of the future versions of MultiCharts.

I agree that Multicharts needs to get its act together. This is the third issue on their end that needs fixing and its quite frustrating having to deal with such issues, especially for the price that they charge. It seems the current state of Multicharts does not work for crypto trading.The fact that MC herself does not respond in threads like these, really does not help.

An extension to the anomalies I encounter myself regarding this, is skipping (hence apply a return) all the bars/calls which are beyond the current date and time. Pseudo code :

**): an Input of the time today which is e.g. 3 minutes past when you start the Strategy, allowing for all the bars in the cache to be skipped up to the current point in time.Code: Select all

if (Bars.DateTime < DateTimeOfInput) // DateTimeOfInput = ** return;

I can't tell how this cooperates with your situation of necessary preloaded bars for calculating averages etc. which may require x minutes as well, and which must be allowed to calculate.

Again I realize how vague this all is to explain. But it is MC who needs to have their act together in the first place. I can only hope this helps you.

-

HellGhostEvocatorX

- Posts: 144

- Joined: Feb 10 2022

- Has thanked: 68 times

- Been thanked: 23 times

Well, only certain character lengths fit into a variable, and since there are no cryptos with such incredibly small values when creating multicharts, I think it's understandable that this isn't implemented. A prominent example is the Berkshire share, which required a change for many stock exchanges because they did not require more than a 32-bit format.I agree that Multicharts needs to get its act together. This is the third issue on their end that needs fixing and its quite frustrating having to deal with such issues, especially for the price that they charge. It seems the current state of Multicharts does not work for crypto trading.The fact that MC herself does not respond in threads like these, really does not help.

An extension to the anomalies I encounter myself regarding this, is skipping (hence apply a return) all the bars/calls which are beyond the current date and time. Pseudo code :

**): an Input of the time today which is e.g. 3 minutes past when you start the Strategy, allowing for all the bars in the cache to be skipped up to the current point in time.Code: Select all

if (Bars.DateTime < DateTimeOfInput) // DateTimeOfInput = ** return;

I can't tell how this cooperates with your situation of necessary preloaded bars for calculating averages etc. which may require x minutes as well, and which must be allowed to calculate.

Again I realize how vague this all is to explain. But it is MC who needs to have their act together in the first place. I can only hope this helps you.

But if you have already received a positive answer from mutlicharts, that is a good answer. I'm keeping my fingers crossed that this happens quickly